Growth options

There are very many reasons (good or sometimes questionable) why a company would seek to grow.

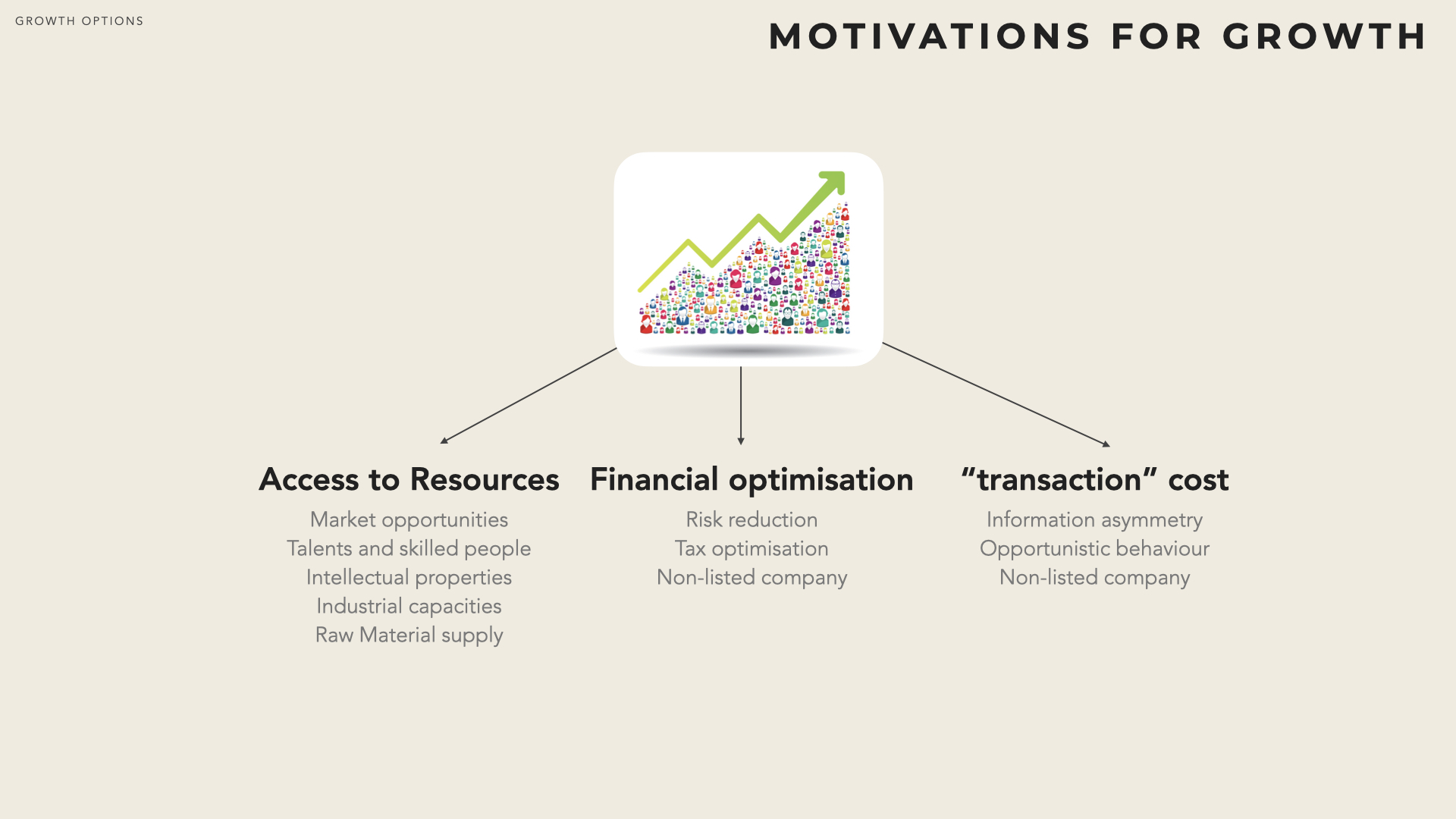

Growth motivations

If we forget fashion effects or ‘prestige’ motivations it all fall down to three major aspirations:

Getting access to resources that the mother company needs and that cannot be obtained efficiently from markets

Financial optimisation that will mostly appeal to Financila investores by also sometimes to CFOs of large coorporations

Avoid transaction costs where uncertainty is such that a contract cannot be establish efficiently.

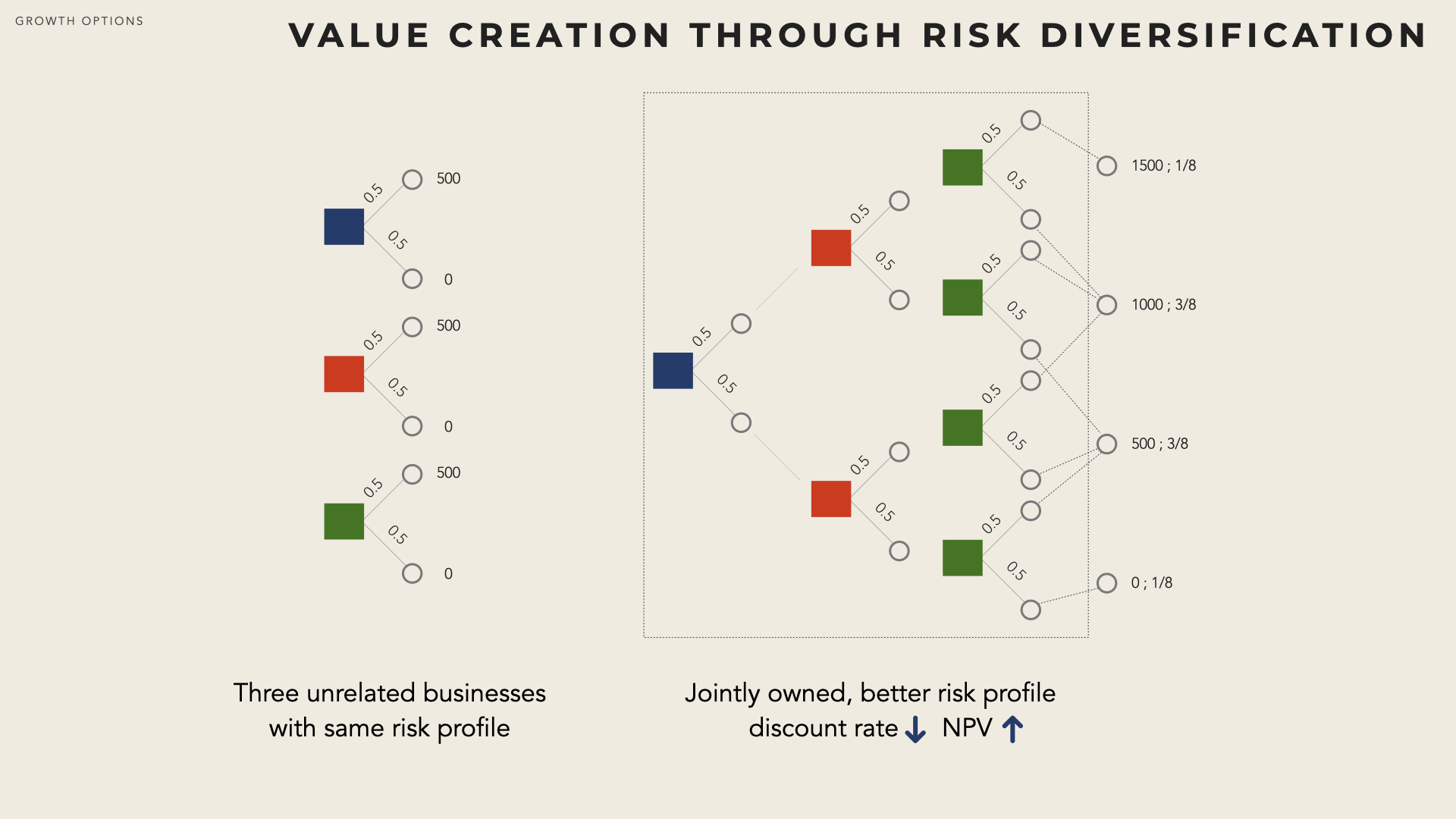

Value creation by risk diversification

Two types of players are involved in Corporate Strategy : financial investors (assemble portfolio i.e. acquire cash flow rights over returns but with limited decision rights) and strategic investors (operate and modify the acquired businesses).

You can create corporate advantage through selection of a good business portfolio (risk diversification). For instance if you have three businesses with equivalent risk profile (in each period, they can yield 500 with a 0.5 probability or nothing).

Assuming that the risks are unrelated, associating the three businesses reduces the overall risk profile: the average return is unchanged while extreme payments are less likely.

As risk decrease, so does the overall discount rate and therefore the value (in terms of NPV) increases.

In addition to create value by risk diversification, a financial investor can typically:

Buy an under-evaluated company (a bargain) and resell it at its true value,

Buy a company and sell it in parts when the sum of the part is less than the parts (diversification discount),

Buy a company, have it restructured and resell it

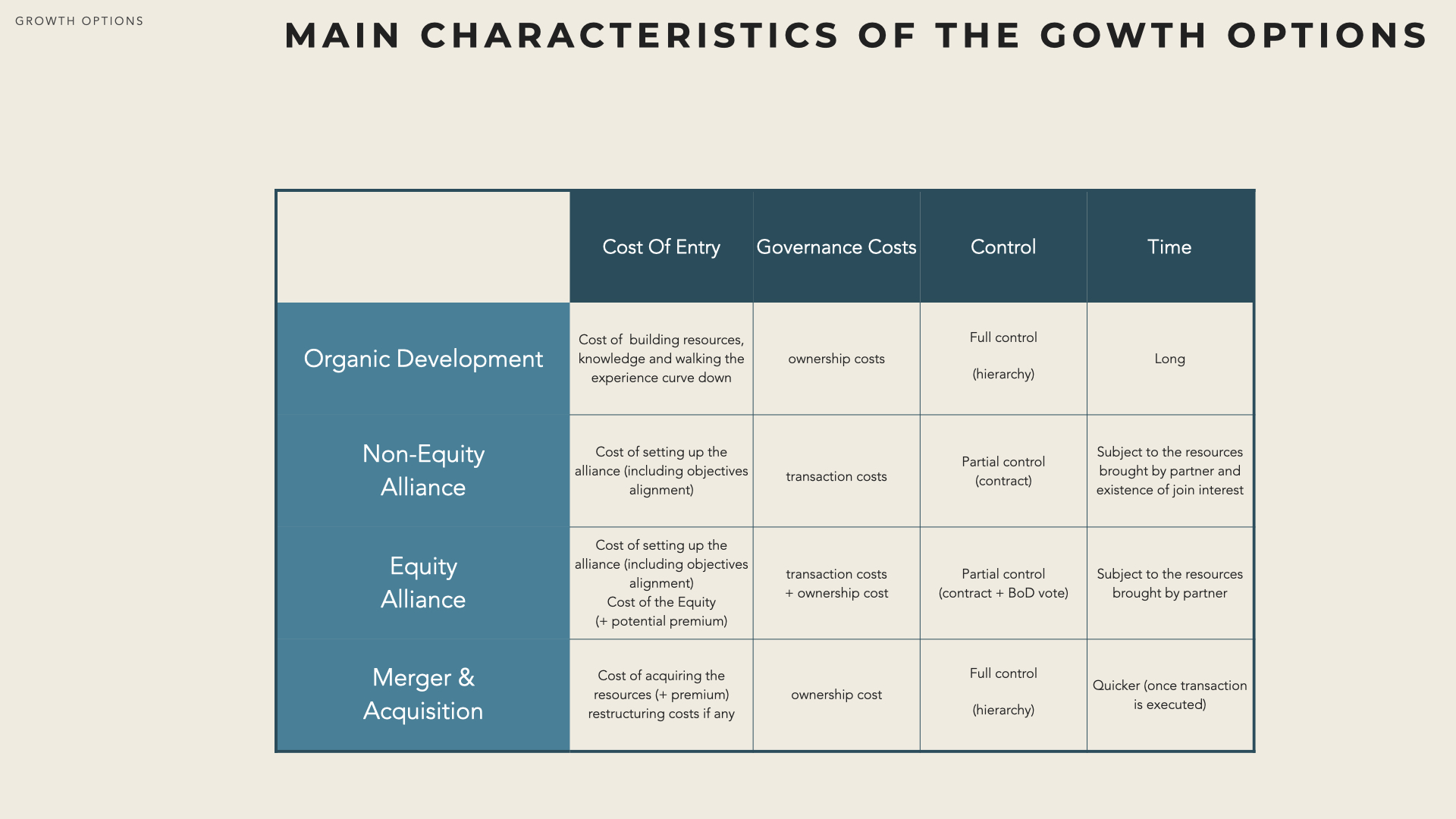

Growth options

In real life the distinction between the various options are not as sharp as it may seem. In addition, depending from the perspective (i.e. legal ) moves may be interpreted differently.

While there is no absolute method to select the optimum path, the following is generally relevant:

1- Identify capability gaps clarify what are the resources that don’t exist (or don’t exist in sufficient capacity, or which performance must be grown) in business A.

2- Assess organic options quickly determine feasibility and rough order of magnitude of the costs.

3- Scan potential targets for inorganic growth if there are bargain go for the deal.

4- Assess expected benefits and costs for the various inorganic options. This is usually done a the level of value chain segments.

5- Compare the options and select the preferred trajectory.

Strategic alliances

The term Strategic Alliance corresponds to a broad concept encompassing a variety of situations where two or more companies set a formal or informal agreement to pursue a join & shared objective.

An alliance is a form of collaboration where each partner contribute strategic capabilities (assets, knowledge, reputation) to a project.

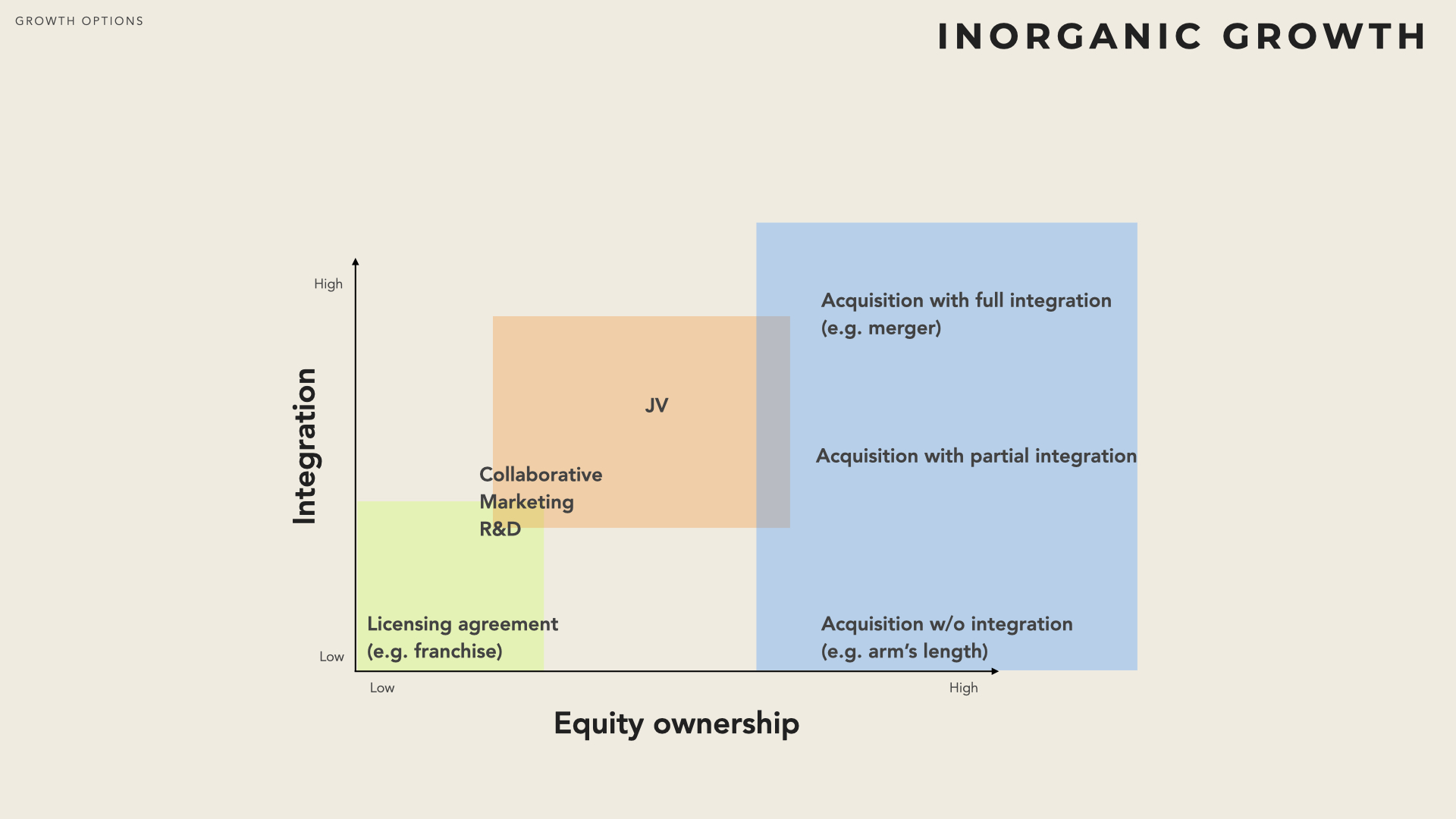

An alliance can be established through

non-equity alliance partners remain independent legal entities. A contract defines the roles and responsibilities of the parties toward a join objective.

equity ownership partners own stakes in each other (e.g. Renault owns 43,4% of Nissan and Nissan owns 15% of Renault). In addition partners will have representatives to each other board of directors. Not all cross shareholding correspond to equity alliances. Indeed an alliance requires the will to collaborate to a join project.

joint venture a new independent company is established and co-owned by the partners.JV are both a form of collaboration and a form of M&A. Sometimes, JV are not considered strategic alliances as resources are pooled in a separate new legal entity

Strategic alliances can be characterised according to whether or not partners operate in the same industry:

horizontal strategic alliance are formed by companies active in the same business area (e.g. Nissan Renault, Airline alliance)

vertical alliance collaboration between upstream and downstream players in the same value chain.

intersectional alliance partners are operating in different markets and control very different resources and competences. They were not connected by a vertical chain or worked in the same business area.

Likewise strategic alliance can be characterised according to the nature of the strategic objective that triggers collaboration:

Coalition based alliances partners –usually from the same industry – seek to achieve global presence, improve their market position and increase their market power compared to other competitors.

Co-specialisation alliances partners combine their complementary expertise to develop and market new product / services.

Learning alliances partners join forces to develop new technologies or solve technical issues.

By and large, collaborations cover one or more of the following purposes:

Technology development improve technology or develop know-how.

Operations & Logistics build economies of scope / scale.

Marketing & Sales distribution infrastructure, affiliate marketing, franchise, licensing.

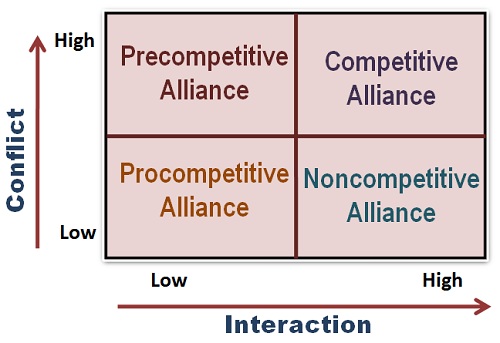

Yoshino and Rangan ( [Yoshin95] ) consider that strategic alliances are significantly influenced by the Extent of organisational interaction (how much must the partners interact to have the alliance work effectively) and conflict potential among the alliance partners (particularly if partners are also competitors in the market).

Four situations may arise:

Pro-competitive Alliances corresponds to low interaction and low conflict. It typically reflects a relationship between a manufacturer and its sup- pliers or distributors.

Non competitive Alliances are characterised by high interaction and low conflict. They are formed between the companies that but do not consider each other as rivals (even if they operate in the same industry) for the purpose of the alliance. Geographical expansions often rely upon such alliances.

Competitive Alliances are characterised by high interaction and high conflict. Partners perceive each other as rivals. Technology development, market access or offsets are typical reasons for establishing such alliances

Pre-competitive Alliance corresponds to a situation with low interaction and high conflict. Typically it can be a partnership between firms from different, unrelated industries who join forces towards the development of a new product or technology.

Synergies

Synergies the holly grail

While a financial investor can only impact the discount rates by reducing and diversifying risks, a strategic investor can change future cash flows (e.g. by increasing revenues or decreasing costs) or their timing.

Without the prospect of synergies and efficiency gains, take-over costs couldn’t be off-set.

Operational synergy means that two businesses operated jointly (decisions are coordinated) are more valuable than operated independently. This can sometimes be achieved through strategic partnerships, but usually requires common ownership.

Synergies can stem from:

leveraging resources improved allocation of resources (transfer resources across business units where better uses can be made of them), replication of existing resources (intangible resources - knowledge, know-how, brand - can be copied from one business to another),

aligning positions improved bargaining position (particularly when products and complementary and can bundled) improved competitive position,

integrating activities value-added activities sharing(e.g. logistics, procurement, HR, legal, value-adding activities linkage (vertical integration / internalisation/insourcing).

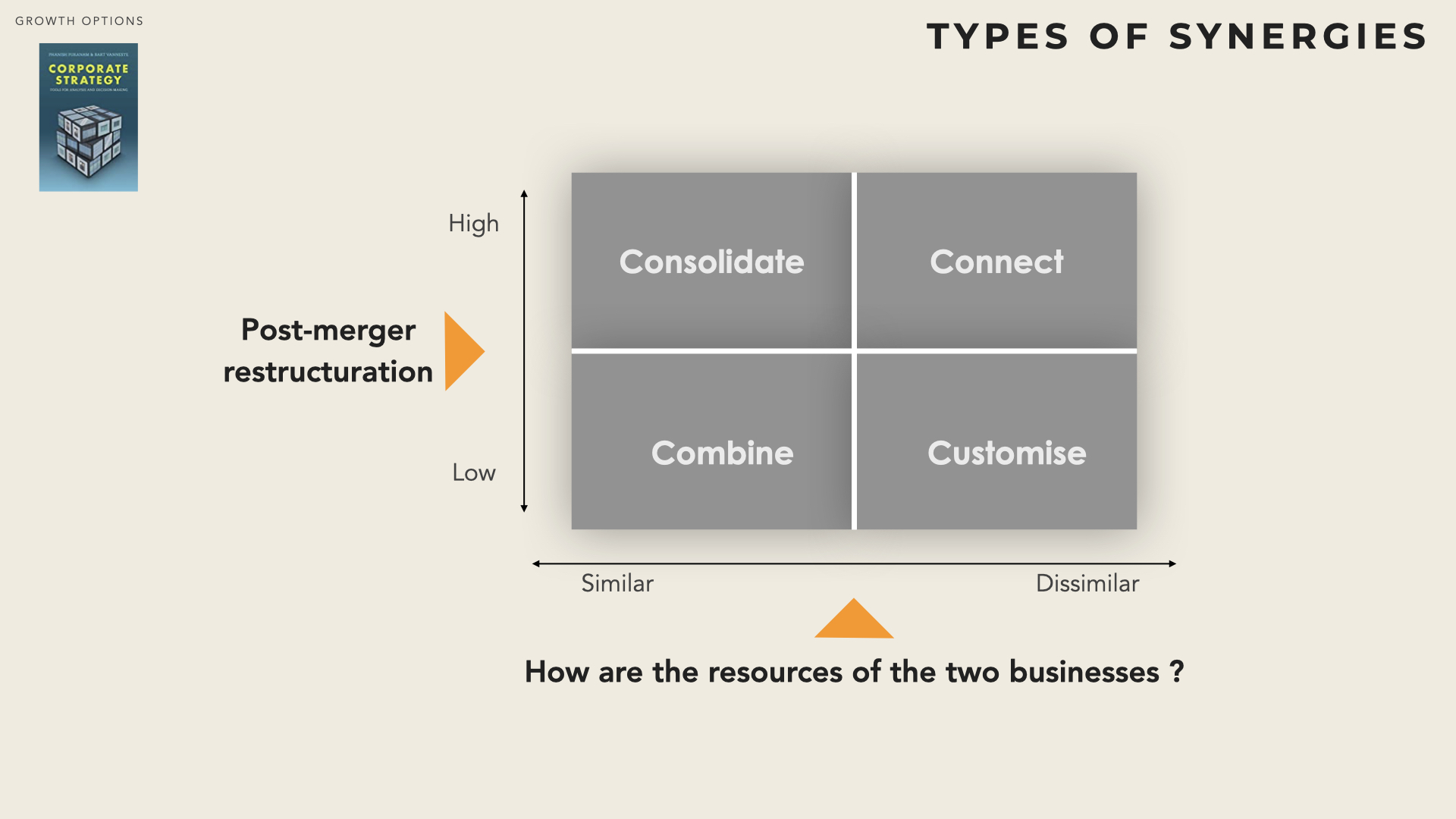

Operational synergies can be characterised according to two dimensions: the level of similarity of the underlying resources (are we linking similar or dissimilar resources when two businesses are jointly operated) and the required level of restructuring.

Similarities: if resources are very similar (at the extreme identical i.e.in case of horizontal merger), then economies of scale might be experienced which will translate into higher performance and value creation. If resources are somehow related, while not strictly identical, economies of scope are likely to be experienced, which again can translate into value correlations. If resources are very distinct (e.g. conglomerate merger) then it might become more challenging to generate higher performance by operating the two businesses together. Complex value chains can exhibit partial similarity (e.g. similar retail networks) while being different at the same time (dissimilar R&D).

Restructuring the extent of modifications and post-merger changes (integration frictions) that is required to operate jointly the two businesses (e.g. suppress duplicate, integrate processes or information systems). The more change is necessary, the more it is likely to inhibit the value created by the synergies.

Assessing actual levels can be extremely challenging (particularly pre-deal for businesses that are insufficiently known / understood ).

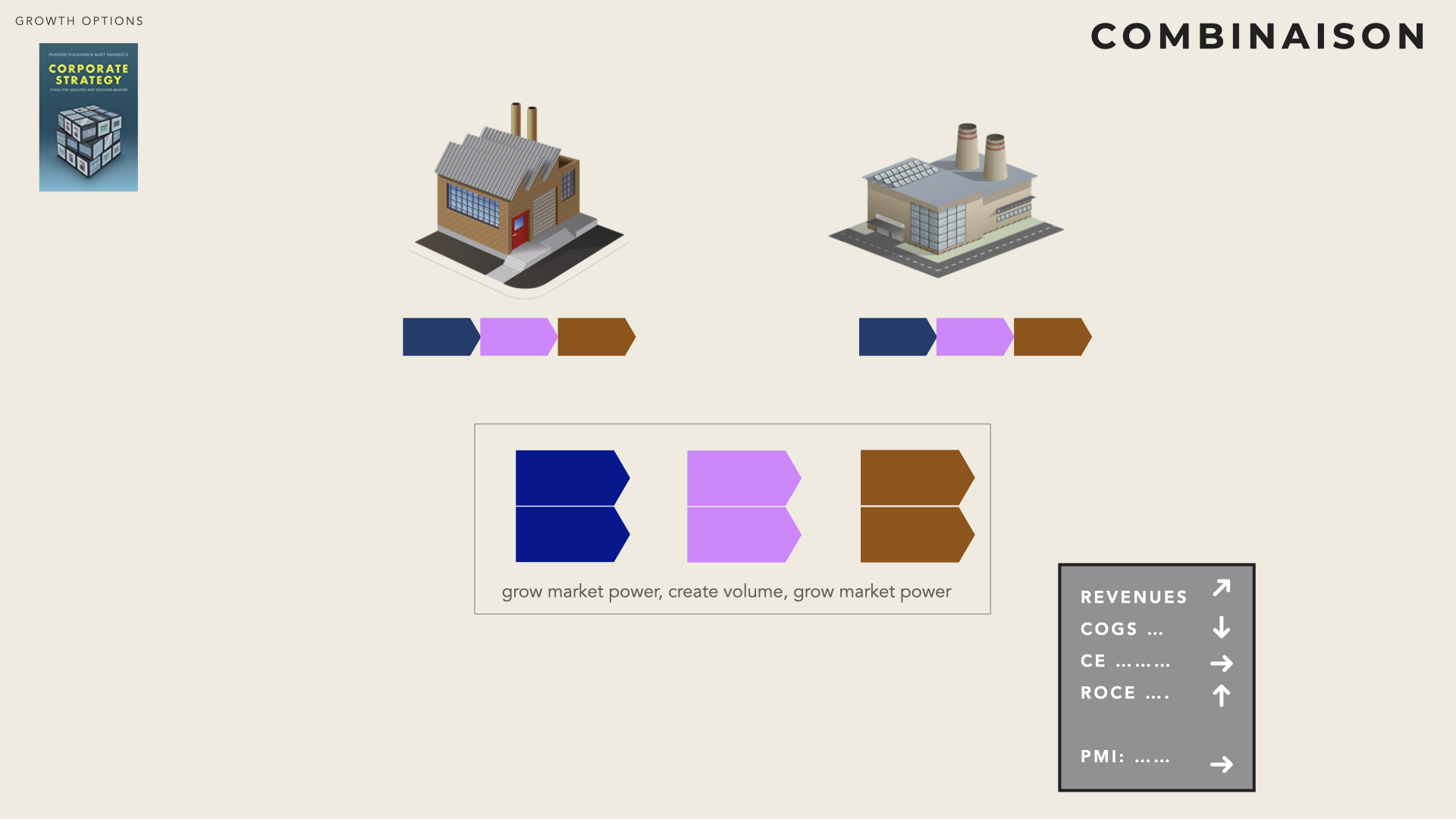

Combination

The two firms have similar value chains and rely on rather identical resources. Post-merger restructuring will be limited (horizontal integration without restructuring). The two businesses will continue to be operated in parallel.

The main objective is to develop horizontally and grow production volume (or limit competition):

If the industry is subject to economies of scale, production costs will decrease with volume

As volume grows the bargaining power with suppliers increases, which translates into higher purchasing discounts and lower costs

When the size becomes significant, incumbent players may compete less, out of fear of retaliation. This will usually allow the company to raise customer price.

Political influence grows with size

HQ usually becomes more powerful (shared services, internal consulting, planning & coordination).

Regulators are vigilant and may block such combination on anti-trust ground.

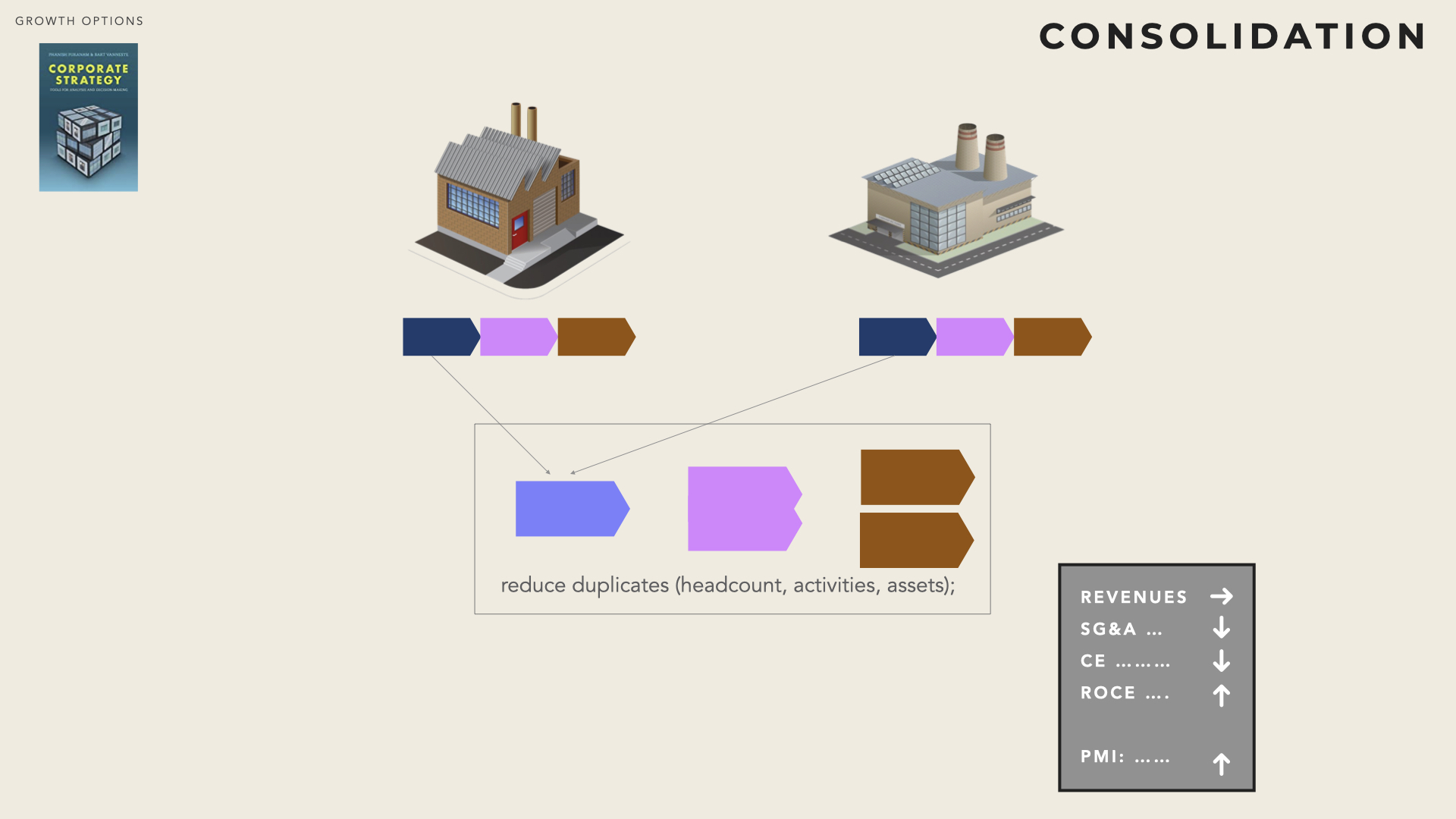

Consolidation

The two firms have similar value chains and rely on rather identical resources. However existing redundancies must be eliminated through restructuring (horizontal integration with restructuring). Synergies are mainly created by rationalisation of duplicates and elimination of capital employed:

Existing non-productive activities (e.g. HQ, IT, Procurement) are merged and simplified (headcount reduction, site closing) - gains are derived from elimination,

Mutualisation is promoted (e.g. shared service, reduction of warehouses and plants if feasible) - for instance factories are run at their maximum capacity and any spare capacity is closed.

Strategic decision-making is centralised as well as corporate finance (e.g. treasury)

As a result, the level of operating costs (mainly indirect) as well as the level of capital employed are reduced. Mechanically the ROCE improves.

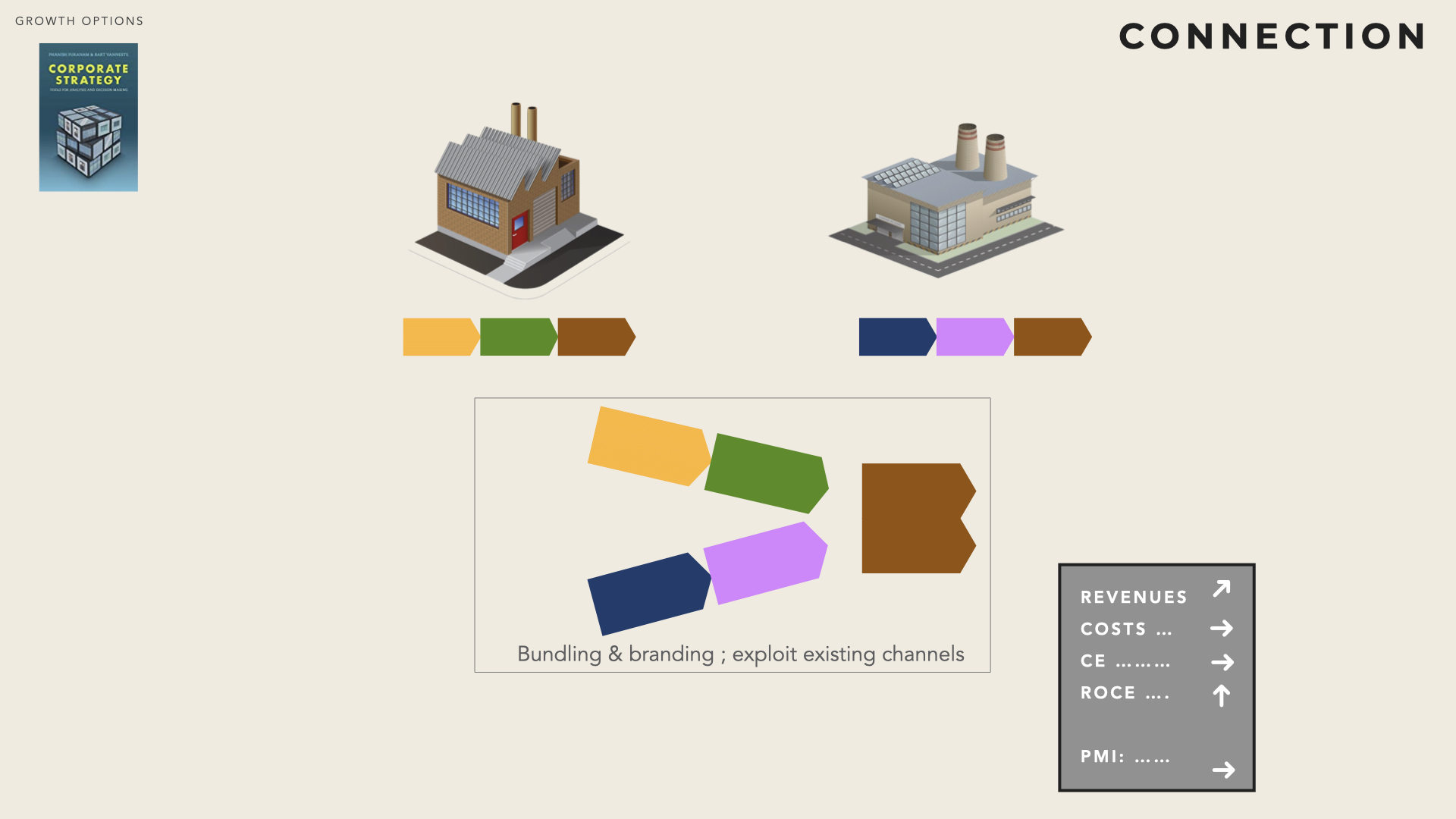

Connection

The two firms have distinct value chains but address similar market segments. The objective here is to complement the value propositions (bundling) while minimising the need for restructuring.

Offer ‘one-stop-shoping’ to customers, which usually grow their Willingness to Pay and the volume of sales.

Exploit and mutulalise existing channels (cross-selling)

single branding and image

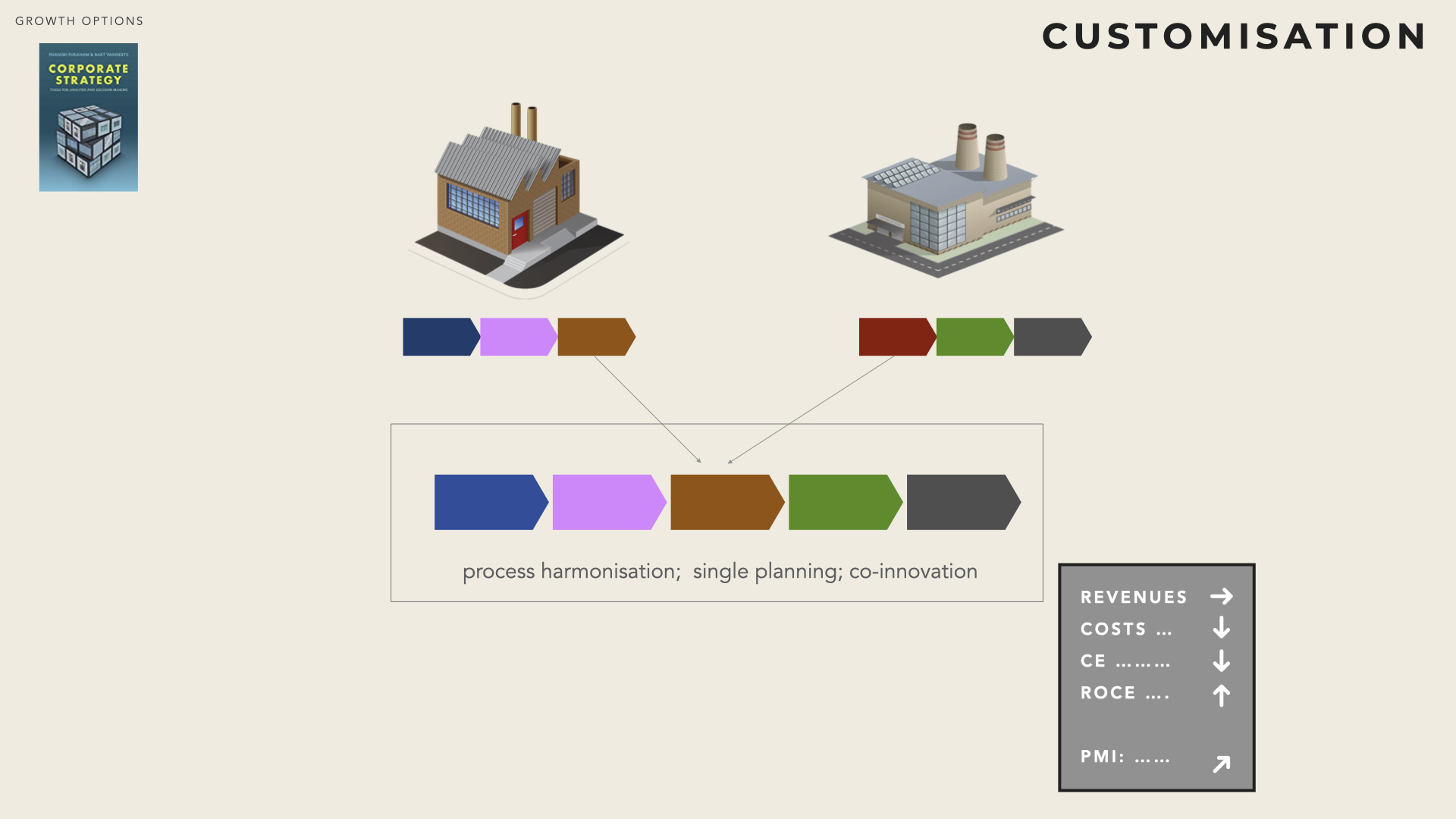

Customisation

The two firms have distinct value chains that contribute to a single value system (vertical integration). The businesses will be operated jointly (e.g. tight planning control) and therefore some restructuring is mandatory (e.g. way of working, management system, finance controlling)

vertical integration and establish process continuity (e.g. planning)

process harmonisation (quality measure, information systems, inventory)

shared resources (warehouse management, HR, Finance)

shared intangible know-how (operations improvement, innovation, best practices)

HQ is usually strengthened

Governance costs

Potential synergies won’t materialise spontaneously. Specific actions (and therefore associated costs) must be carried out to grow cooperation, operate two businesses jointly and realise the synergies.

Governance costs are called ownership costs, when the two businesses are jointly owned and transaction costs, when the two businesses are operated jointly but not owned jointly. Transaction costs also occur in standard customer-supplier relationships.

Synergies can be one-sided (only one business will measure gains) or two-sided (the performance of two businesses will improve).

Governance costs tend to be higher when restructuring is needed and when synergies are one-sided (due to the asymmetry of incentives to cooperate).

Other post-integration costs can be incurred such as i) brand dilution, ii) organisational complexity, iii) suspicious of private information leakage (when the two firms were previously competing), iv)anti)trust-obligation. These costs are sometimes called dys-synergies

Make, Acquire, Team

Inorganic growth options

The choice to team with (partnership) rather than to buy (acquisition) a business can be driven by regulation (e.g. in countries such as China, India Canada, Foreign Direct Investment is restricted and cannot reach 100%).

When the fate of the two players are tied (they will win or loos together) a non-equity alliance can be sufficient. It is noteworthy that the relation customer-supplier relationship can be so close that it resemble a non-equity alliance.

Taking a minority equity (acquisition or partnership) can discourage the competitors of A to also form strong relationships with B. It also creates the option to later strength the equity participation.

Acquisitions

M&A becomes the right pathway when i) the firm has identified and made explicit the strategic rationale for the move and ii) all alternatives options have been ruled out (e.g. the firm lacks the internal skills and resources to build in- house and as no effective contractual relationship can be established with a partner then a full control over the partner is required).

There are three main ’flavours’ of resource combinations that can be brought by M&A:

Exploitation the acquired company brings resources that complement and strengthen the core domain of the firm, which enhance its existing activities in its established markets

Extension the acquired company facilitates the development into new markets (geographic, new customer groups, etc) or provides additional products / services that can be offered to existing customers.

Exploration the acquired company allows exploring new market-spaces, potentially through disruptive technologies, products or business models.

When carefully chosen, priced and executed, M&A help firms create value by providing access to new technologies, exploiting learning opportunities, meeting customers’ needs, exploiting economies of scale or restructuring industry capacity.

The difference between ‘Merger’ and ‘Acquisition’ can be subtle (furthermore lawyers and accountant often have diverging views here). By and large, when a company B is ‘merged’ it ceases to exist and it is encapsulated within A (or a new company into which A is also merged). An ‘acquisition’ corresponds to A taking ownership of B’s stock (shares), equity or assets.